Take Control of Your Finances: Get Organized in 2026

Does your financial life ever feel overwhelming?

If so, you’re not alone. Between rising costs and the ever-increasing digital complexity of modern life, many Americans are feeling the pressure.

The good news is that small steps toward organization can make a big difference. When you streamline your financial information and create simple routines, you build confidence, reduce stress, and gain a clearer picture of your financial future.

Get Organized at Home

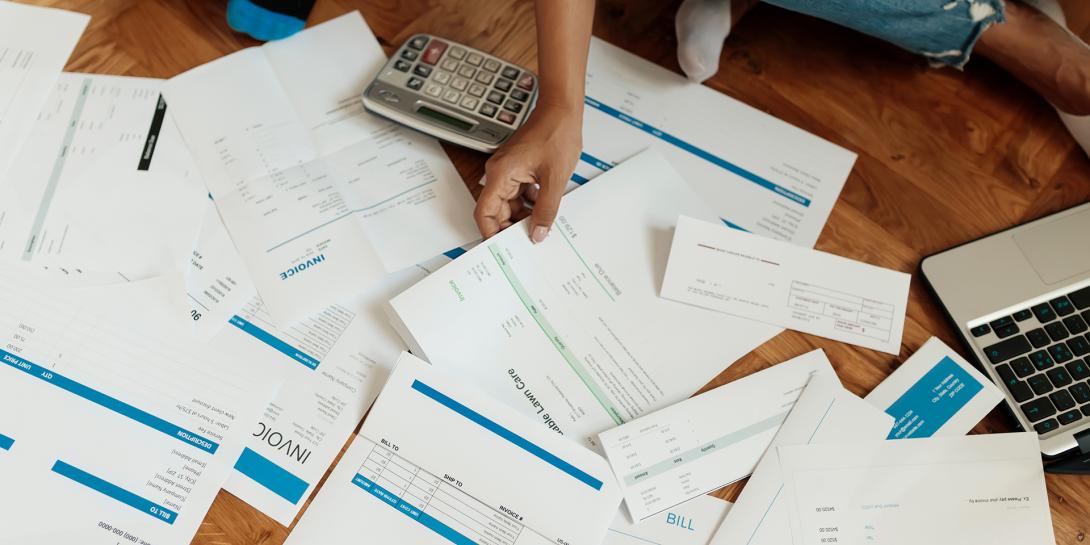

Organization is always easiest when you start with the basics. Start by organizing your physical and digital financial documents at home.

- Pick one place to keep your documents. If your screenshots, emails, and paperwork are scattered across different locations, it becomes difficult to find what you need when you need it. Choose a single system—digital or physical—and stick to it. We recommend arranging all your files in one location organized by account and date.

For digital folders, scan or photograph physical documents to store them electronically. If you prefer a file cabinet, print important digital records so everything is in one place.

Always keep security in mind: set a password for digital files or invest in a lock for physical storage. You do not want unauthorized individuals accessing sensitive information. - Create a routine for handling important correspondence. Decide whether you will address incoming messages each day or prefer to tackle everything once a week. Choose what works for you and follow it consistently.

- Stay alert to potential scams. Keep a clear head when reviewing bills and important documents. Scammers often impersonate authorities, businesses, or service providers and may send spam attachments, fake notices, or other fraudulent communications.

Declutter Your Finances

Remember when your biggest financial decision was how much to save from your part-time job? As life becomes more complex, your finances do too, which can make everything feel disorganized. Take this opportunity to simplify with the following steps:

- Review your accounts and see what you can close or consolidate.

- Bank Accounts Most people don’t need several checking accounts and savings accounts spread across various financial institutions. Review the benefits of your accounts and close those that no longer suit your needs.

- Credit Cards While it is not usually advisable to close unused credit cards since they affect your credit history, that does not mean you need to use all of them. Choose a primary card for everyday spending and aim to pay off the balance in full each month.

- Retirement Accounts: If you have a retirement account from a previous employer, talk with your financial advisor to determine whether rolling it into your new employer’s plan or another qualified account would be beneficial. Consolidation can make it easier to track your long-term savings.

- Payment Apps: Consider whether you really need all the payment or “buy now, pay later” apps you have downloaded. Select one or two you prefer and close the others. Keeping your information in fewer places reduces risk and simplifies tracking your transactions.

- Subscriptions: Review all your subscriptions. If you cannot remember the last time you used a streaming service or visited that gym, it may be time to cancel. You may even discover subscriptions you forgot you signed up for—or duplicates for the same service.

The fewer accounts and platforms you maintain, the easier it becomes to stay organized.

- Take advantage of direct deposit from your employer, if available.

Arrange for your paycheck to automatically deposit into your checking account, savings account, and retirement account (if not already handled through payroll deductions). That’s three financial tasks completed every month without any extra effort.

- Automate your recurring payments. Save time and avoid missed due dates by setting up automatic payments for regular bills. PinnPay Online Bill Pay offers a secure way to pay digitally, which is safer than mailing checks—a common target for fraud.

Manage Financial Goals

Keeping your financial life organized also means setting and working toward meaningful short- and long-term goals. Use this cycle to stay on track:

- Track your spending. Monitoring where your money goes helps you understand your habits and forms the foundation of effective budgeting.

- Create a budget that supports your goals. Whether you’re saving for a home, a new car, or a family vacation, begin by determining the cost. Then review your spending to identify opportunities to adjust your habits and save more intentionally.

- Consider the 50/30/20 rule for budgeting. Many people find this approach helpful: allocate 50% of your income to needs, 30% to wants, and 20% to savings and debt payments.

- When you reach a financial goal, set a new one. Consistently having a financial goal keeps you motivated and engaged. If you want to feel more in control of your finances, always have at least one objective you are working toward. Need more tips? Visit our Resource Center for more tools and guidance.